What I don't understand is why you have such faith in the market yet blame the government for out of control capital gains. That is the free market.

I'm saying the exact opposite. The current situation has arisen out of the opposite of a free market. CMHC protecting banks from risk, instigating 5% down 40 year loans, setting interest rates artificially low. These are all controls that have driven the market out of control and have nothing to do with a free market environment. Australia offering $28K grants, extending amortization; it goes on and on in just about every country. This is why property has created such speculative interest internationally. It wasn't this way prior to this.

As for the rental crunch in Squamish the council needs to get the developers to build rental only apartments. They can do this when they are seeking approvals for their variious projects. The BC gov could also impose the protection on rent increases in the tenancy act to fixed term leases so that newcomers with more money can't displace current residents. Seeing as it is the people that can afford the least that are being squeezed this should do a lot to help, but at the end of the day Squamish has become more expensive and there will be some pains. All I am saying is that with the protection of the tenancy act people that rent would have not be forced out in the first place and there is still plenty of opportunity for the landlords to make money. You keep mentioning the 20% mine was increased, but it was 25% and if they listened to Century 21 it would be 40%. Hell it could be 100%, there is nothing to stop them from doing this and these people actually use the basement suite on weekends and have to face me so I imagine that is the only thing that stopped them from going with the 40%.

I would have to say I am coming around to your idea that having increases capped on fixed term leases has merit. I would argue however, that fixed terms have been popularized just as much because it's way too hard to evict a shitty tenant, and not just so they have the option to jack the rent.

Regarding your suggestions that the developers need to build rental only units, do you mean putting in a % within a larger complex? Who will own and manage these; are you talking state owned social housing here? Are you talking whole buildings? Not saying any of these are a bad idea. In fact, mixing low cost housing within larger projects is a good way to mix demographics. I also think suites are even better at mixing demographics and should be encouraged. But if the developer loses out by making these, then that will push up prices to purchase for the rest and we need strategies to bring prices down. It's a tough situation to solve, but bottom line is we need more housing stock of every kind and I think the best way to do that is reduce barriers to entry. The fact that it's taken years to get the Oceanfront off the ground doesn't help increase stock. And from what I hear, this is how the district rolls.

1 - I didn't make any of these assumptions.

2 - Housing value rarely doesn't outpace inflation.

3 - I don't know what the market was at, but even if you paid 75% of the guys mortgage he was still probably making money and almost certainly would have if he hung on to it. Paying for the house isn't an expense so the rent doesn't need to cover it to make money, You could make the argument that it should pay the interest, but you keep implying that there is a net loss when the rent doesn't cover the mortgage.

4 - If the bubble bursts and my mortgage goes under water what does that have to do with renters? Good for them, they can laugh all they want. I bought what I can afford and will weather the storm.

1. Maybe I misinterpret you, but when you say

OMG, he wasn't losing money. If he bought a house in Squamish he was making money. End of story.

when referring to a time when there was capital depreciation, not appreciation it makes me think you forget that values can go down. Indeed they always have in the past when bubbles burst, even in Vancouver in the past.

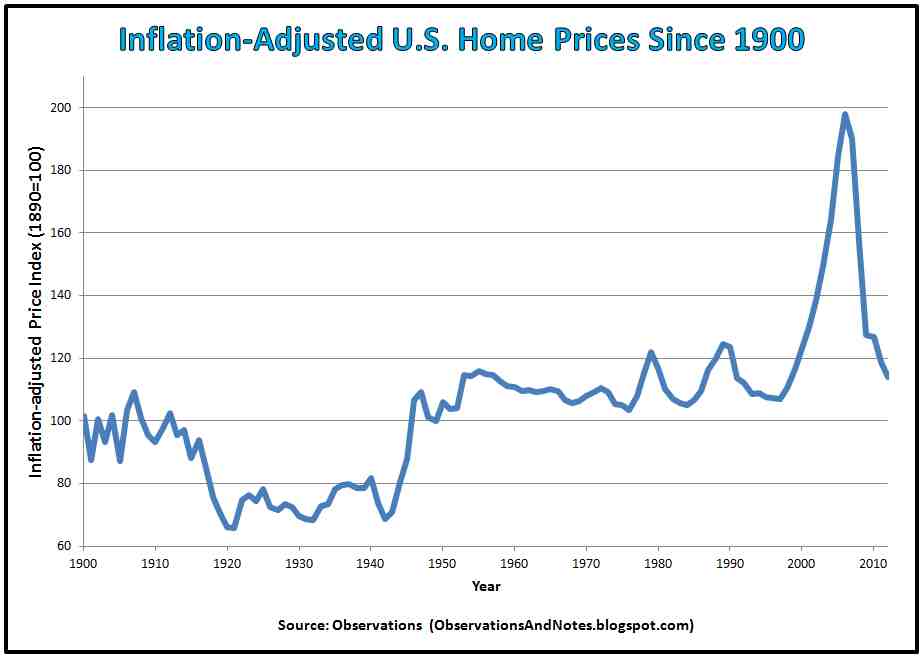

2. Housing values historically have not outpaced inflation. See this chart for US numbers, but the same is true for other countries. Outpacing inflation has always reverted to mean after the bubble bursts. As you can see the values in 1995 are almost the same as 1900 (maybe 20% in 100 years) Nothing like what we have seen post 2000. http://4.bp.blogspot.com/-kjOHoEKbH7A/ULQgiAZ45RI/AAAAAAAABh4/8U-RJx1-pGg/s1600/Inflation-Adjusted+U.S.+Home+Prices+Since+1900.jpg

3. Yes, you are correct. When I say mortgage I really mean mortgage interest. And if it was paid in cash I mean opportunity cost.

4. I am just making a point that renters are protected from loss in such a situation. With tight controls they are protected in up markets and down. Yes, owners have made out like bandits in the last 10 years in Vancouver, and in the last 3 years in Squamish, but this is an anomaly. For the 4 years before that in Squamish they were certainly not. I'm sure everyone has seen this chart and can infer that this is a gigantic bubble and not a normal situation. http://www.mikestewart.ca/wp-content/uploads/2016/02/January-1977-to-2016-REBGV-Price-Chart-Mike-Stewart-Vancouver-Realtor.jpg

It should be noted that these numbers are not inflation adjusted which is why it appears prices have outpaced inflation from 77 to 97.

{kind=link}

{kind=link}